The interest in impact investing has been growing at a highly accelerated pace. As for global assets under management, impact assets have grown at a 12% annualised rate between 2015 and 2019 [Global Impact Investing Network 2019]. Institutional Investors who are keen impact champions want their investments to provide a positive social and environmental impact, whilst pleasing shareholders by maintaining risk adjusted returns. Hence as a result, championed impact investors at both institutional and asset management levels have the additional objective of maintaining ‘impact’ alongside risk and return.

Within traditional portfolio management, methods for portfolio optimisation are used to determine where the trade-off between risk and return are best optimised. However, these traditional portfolio management methods are not designed to add the third factor: Impact. As a result, investors have used the traditional portfolio allocation rules and strategies to allocate mandates to impact funds. The most simplistic approach is view impact assets in the same light as traditional assets and carve out a percentage of their assets to dedicate to impact investing. [1]

Defining impact is important. According to the Global Impact Investing Network (The GIIN), impact investments are defined as: “investments made with the intention to generate positive, measurable social and environmental impact alongside a financial return”.

Expected financial, social, and environmental returns from impact funds vary. However there lies a general misconception that Impact Investing targets below market rate returns, which is false, and academia even argue that impact investing can add financial value. However, some impact funds that lean greater toward philanthropy invest in areas which one cannot expect market returns, and some investors will trade lower returns for greater impact.

However, many investors are still curious of the concept, yet question if achieving measurable positive impact can coexist with strong financial returns or if there is sacrifice for these earnings for contributing to good.

This balance is complex and has many different factors to consider. Concluding on an answer must be backed by historical research and a foundation of knowledge for the various aspects of impact investing.

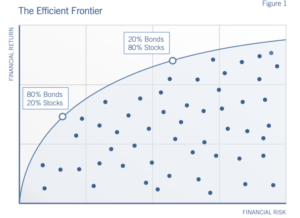

For Investors and Portfolio managers who learnt under the Modern Portfolio Theory (“MPT”), the concept of the trade-off between risk and return is an industry consensus in building a portfolio. The essential principle of MPT is that for higher risk assets, investors will demand higher returns and vice versa for lower risk assets. When applying MPT in carving out a portfolio, it is agreed on that by grouping assets together in a way where we can deliver the best financial return within a given level risk. Upon plotting all these portfolios beside each by risk and return, we develop the efficient frontier. However, for the case of Impact Funds, this does not demonstrate information regarding optimising the social or environmental returns a portfolio may deliver.

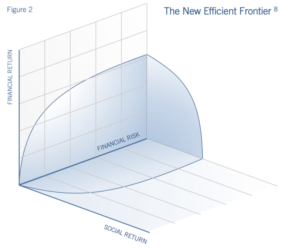

A white paper published by Athena Capital’s Vice President Jeff Finkelman integrates MPT with impact investing, demonstrating a new frontier where Impact is an independent factor that moves along the new efficient frontier like the 2 pre-existing factors. [2]

There exist several views on impact investing. Sceptics call impact investing an investment that provides lower adjusted returns for the same risk as a traditional investment, consequently declaring impact not suitable for portfolio optimisation.

However, WONA believe that impact investments do not always require an investor to accept lower returns for the benefit of impact. Jeff Finkelman’s white paper describes a neutral view of impact investing, demonstrating an investment sweet spot. Within this region, investors can contribute to demonstrable impact whilst not sacrificing risk adjusted returns.

Finkelman states that this point of the curve is where investors can access ‘free’ impact, without increasing risk or sacrificing returns. Nevertheless, impact investing still contains risks alike traditional investments, with risks such as lack of track record and unproven investment strategies as some of the risks that impact managers face.

For Finkelman’s thesis to be correct, it would mean that it is possible to map the effect of where impact starts to take over the effectiveness of financial returns. Based on this curve, financial first investors will either seek to generate greater financial returns without considering the social return of an investment or maximise the optimising financial returns while achieving some impact objectives. On the contrary, there may exist impact first investors who take impact priority over financial returns and impact only which wish to maximise social and environmental returns. [1]

By simply carving out a section of a portfolio for impact can be argued as inefficient allocation method. Forward thinking impact investors will consider the dimension of impact when allocating to an impact investing manager.

A study conducted by Arvella investments demonstrated a methodology to integrate impact funds into a mainstream portfolio while considering the impact of the portfolio. Arvella designed a portfolio optimiser that brought together: risk, return and impact. The study found that the impact funds that were used in portfolio construction had low correlations to traditional asset returns, assisted in developing portfolio diversification and enabled the achievement of greater impact all without harming risk-adjusted returns. By adding impact funds, the optimiser demonstrated that the portfolio could increase allocations to impact funds up to 18% without sacrificing risk adjusted returns.

The study assessed across the asset classes of Equity, Bonds, Private Equity and Private Debt. A range of mean variance optimal portfolios were constructed in mind for investors with different risk limits. This resulted in portfolios demonstrating characteristics of high volatility, selected by risk inclined investors comprising of only public equities and private equities and lower variance, which comprised of bonds and private debt.

The study then constructed new portfolios with impact funds now into the equation. In this study, impact funds were allocated 10% of the portfolio. In this example, the proportion of impact funds were divided into 25% private debt and 75% private equity, reflective of the impact investing universe as of the GIIN’s 2020 impact investing report. In the final allocation, the study looked to maximise impact allocations, without financial sacrifice. The study demonstrates over the standard volatility range, 5% to 15% the proposed optimisation strategy delivered a noticeable increase in impact fund allocation, +10% to retain expected return and volatility consistency and +18% to maintain portfolio utility. Additionally, the study also demonstrated that increasing allocation from 10 to 11.8% (1/5 increase) will have no effect on risk adjusted returns. [3]

An additional effect of allocating to Impact Funds is the benefits from diversification and subsequently low correlation to broader debt and equity markets. The attractiveness of Impact Funds, especially debt strategies is that they provide balanced returns, and low correlation with traditional asset classes. The nature of this asset class benefits in maximising impact whilst keeping expected return and volatility.

From the studies overview, impact funds with proven strategies and achieve at-market and above market returns are suitable allocations when considering constructing a portfolio. Progressing the sustainable development goals through impact investing managers, is necessarily correlated with sacrificing risk-adjusted-returns and portfolio utility. Over the universe of impact investing, financial first impact investors and investment managers will understand that generating impact overlaps in producing in risk adjusted returns.

- Botha, F., 2021. Does Impact Investing Always Come At A Price?. [Blog] Forbes. Available at: <https://www.forbes.com/sites/francoisbotha/2020/04/14/does-impact-investing-always-come-at-a-price/?sh=3e6df57d192e>

- Finkelman, J., 2017. Building Impact Portfolios. [White Paper] Athena Capital Advisors, Available at: <https://www.philanthropy-impact.org/report/building-impact-portfolios> .

- The Journal of Impact and ESG Investing, 2021. Integrating Impact Funds into Mainstream Portfolios. Summer 2021(1 (4), pp.103-119. Available at: <https://doi.org/10.3905/jesg.2021.1.020>.